Special Report: Seaport Entertainment (SEG)

SEG is a spin-off that owns real estate in the heart of Manhattan

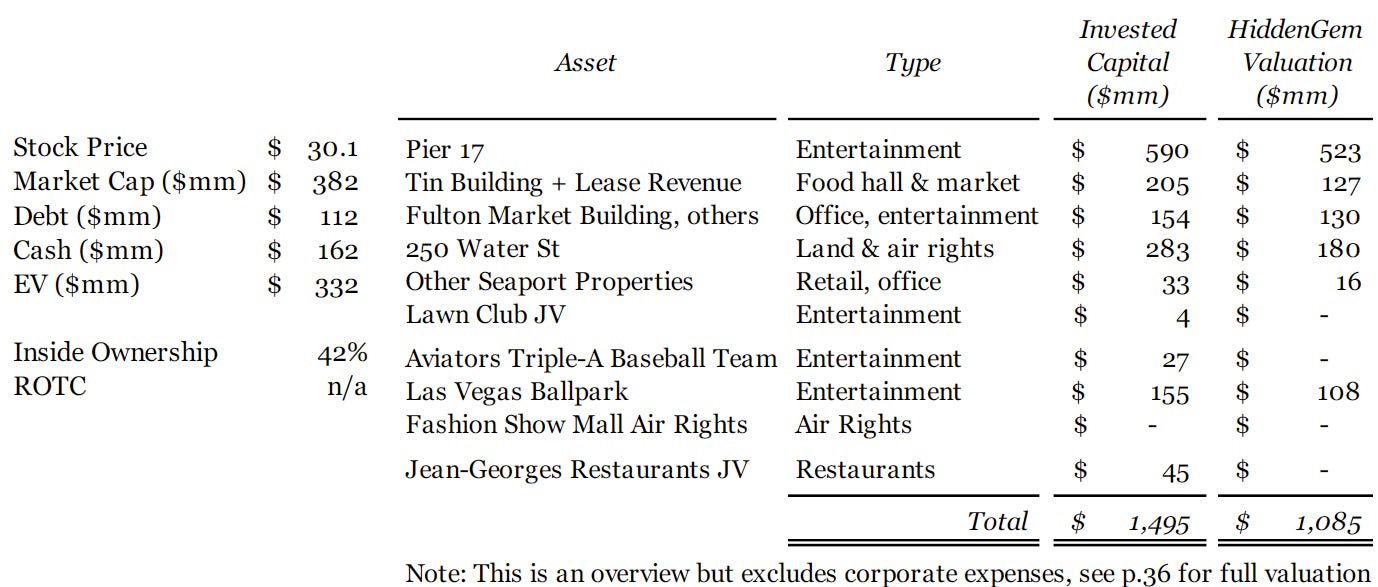

Situation Overview

Seaport Entertainment was spun out of Howard Hughes in July 2024. The company is a collection of complex and loss-making properties in Manhattan and Las Vegas that has dragged down Howard Hughes’ stock for years and was likely sold down by shareholders post-spin.

Insiders, however, are buying shares. Pershing Square owned 38% pre-spin and Founder Bill Ackman was Chairman of Howard Hughes for 13 years, including when the spinoff was announced. Pershing backstopped the post-spin rights offering and increased their stake by oversubscribing to the shares. Seaport’s new CEO and CFO have both moved their families to New York to take up their roles and are largely compensated in stock.

We believe these insiders recognize that Howard Hughes invested ~$1.5bn into these properties and that there is a path to significant recovery. Seaport’s market cap is $382mm and it has net cash. Many of the properties are just 10 mins walk from Wall St, overlook the Brooklyn Bridge, and will benefit from the new management’s background in entertainment and hospitality.

We believe that the company has two properties which have performed well and are worth most of the market cap today, giving us significant downside protection. While the upside is less certain, we think intrinsic value in three years is likely double today’s share price and that we could be at the beginning of an entire neighborhood of Lower Manhattan appreciating in value. That makes an investment in Seaport today an asymmetric risk/reward opportunity.

Key Insights

1. 250 Water St and the Fulton Market Building have values that can be reliably determined and cover most of the market cap. We believe 250 Water St could be sold in the next 12 months and act as a significant catalyst for the stock. (See p. 11-13)

2. Pier 17 could be worth more than the entire market cap. The property has substantial earnings potential and significant improvements are already underway. (See p. 14-22)

3. The Tin Building food hall and market is by far the most problematic property, losing $43mm in 2023. However, similar food halls in Manhattan are profitable and we see a viable path for the Tin Building to do the same. (See p. 23-30)

Research Methods

In addition to utilizing secondary sources such as company filings, transcripts, and services such as Tegus, the information in this report was gathered by speaking with primary sources. This included discussions with:

Seaport Entertainment’s CEO, CFO, and IR

4 former employees at Howard Hughes

4 former or current employees at comparable properties in New York

9 real estate specialists in New York or Las Vegas

2 other relevant sources

Multiple visits to all of Seaport Entertainment’s properties in New York and several comparable properties in New York

We spoke with some sources more than once. Information that could reveal the identity of the sources above are redacted from this report unless sources gave their permission, apart from Seaport Entertainment’s CEO, CFO, and IR given the company is publicly traded. While Hidden Gems Investing gained many insights from these conversations, no information that was both material and non-public was shared.

We think you will enjoy this writeup more in a pdf format. Click “Download” below: